Navigating the Agricultural Landscape: Challenges and Opportunities in a Complex Economic Environment

Donny Rocha | October 2024

A Shift in Producer Sentiment. The agricultural sentiment in the San Joaquin Valley mirrors concerns reminiscent of the mood in 2015, marked by declining prices and increasing operational costs. During that time, producers faced similar challenges, prompting a cautious outlook across the farming community. Currently, sentiment surveys, including the Purdue Ag Economy Barometer, indicate that producers are feeling the strain of economic pressures, particularly from water management regulations and market volatility. Producers are growing uneasy, especially regarding credit availability and investment in the face of tightening margins.

Energy and Transportation: Economic Undercurrents. The agricultural sector is currently facing significant challenges due to a combination of factors, including rising oil prices, water level issues in the Panama Canal, and potential union strikes affecting supply chains. In October 2024, OPEC decided to increase oil production by approximately 1 million barrels/day in aims to stabilize prices. Despite this, oil remains volatile, hovering around $90 per barrel. This fluctuation raises transportation costs for farmers, directly impacting their operational expenses and potentially leading to higher prices for consumers.

Compounding these issues are the low water levels in the Panama Canal, which are causing delays and increased shipping costs for agricultural exports. The canal's limited capacity affects global trade routes, making it more challenging for U.S. farmers to get their products to international markets efficiently. Furthermore, the threat of additional union strikes in key transportation sectors, including ports and trucking, exacerbates these logistical challenges, potentially disrupting supply chains even further.

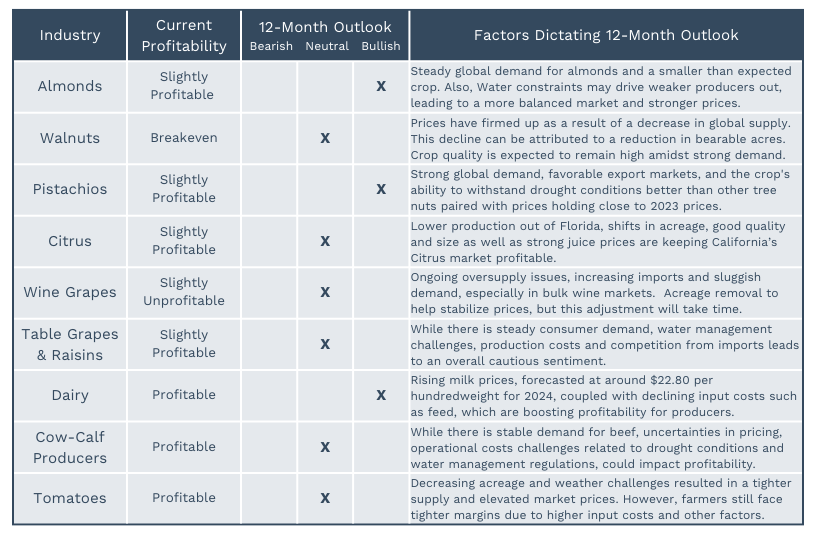

Almonds: Balancing Supply and Demand. The California almond market has seen near ideal harvest conditions, and the crop is expected to come in slightly under the estimated 2.8 billion pounds. That’s good for prices, which have largely continued to firm. Handlers are working to balance supply and demand. Although export shipments have shown some resilience, growing 1.8% over last year, domestic demand is lagging. However, reduced inventory carryover and a weakening U.S. dollar, which boosts export competitiveness, may support prices as the season progresses. Additionally, the implementation of the Sustainable Groundwater Management Plan (SGMA) is prompting some growers to remove almond acres, potentially supporting long-term prices.

Pistachios: Prices and Demand Holding Up. On the pistachio front, growers report favorable quality and size profiles for the 2024 crop. Prices are holding steady at just below 2023 levels, aiding producer profitability. While exports remain robust, especially to markets like China, growers are concerned about sustainability and profitability amid rising production costs and market volatility. With expectations of a large 2025 crop due to the alternate bearing nature of pistachio trees, producers are motivated to sell quickly and minimize inventory carryover. As with almonds, the pistachio market highlights a complex landscape where growers must navigate fluctuating demand, pricing pressures, and external economic factors.

Walnuts: Cautious Optimism. The California walnut market is currently experiencing a notable shift with market prices firming up. The 2024 walnut production forecast is set at 670,000 tons, a significant decrease of 19% from the previous year's record of 824,000 tons. This decline is attributed to a reduction in bearing acreage, down to 370,000 acres from 385,000 the previous year. Despite this dip, the quality of the upcoming crop is expected to remain high, continuing California's reputation for superior walnuts. Additionally, the industry is optimistic about market stability, as preliminary data suggests that the 2023 crop is virtually sold out, indicating robust demand. Overall, while production may be down, the market sentiment remains cautiously positive, bolstered by strong consumer interest and effective promotional efforts.

Citrus: Mixed Market Signals. The California citrus market is currently experiencing a steady state with signs of growth in certain segments, particularly lemons and mandarins. The key factor in this may be a shift in bearing acres. According to the USDA’s 2024 California Citrus Acreage Report, Valencia orange acreage is down 1.8%, while lemons and mandarin acreage is up from 2022, 6.6% and 2.6% respectively. Lemon producers are slightly profitable, but as more bearing acres add to the supply, the upcoming crops may be closer to breakeven levels. The supply of Valencia oranges from Florida was smaller than expected, largely due to diseases like Citrus Greening Disease, which California’s producers have largely been able to avoid through effective management practices. Paired with strong juice prices, this has supported the profitability of California orange growers. Producers are optimistic about this year’s Navel orange crop with favorable size and quality. Overall, while some traditional crops like Valencia oranges are experiencing declines in acreage, the industry is positioned to adapt and grow in key areas.

Tomatoes: Withstanding the Heat. The profitability of tomatoes is under scrutiny amid fluctuating market conditions and environmental challenges. San Joaquin Valley tomato producers are facing reduced yields due to extreme weather, which has led to quality issues and a tightening supply. This, paired with a decrease in planting acreage, has resulted in higher prices, potentially enhancing profitability for growers who can manage the risks associated with these conditions. However, profitability remains contingent on various factors, including production costs, labor availability, and market demand. Thus, farmers may face tighter margins despite elevated market prices.

Wine Industry: Oversupply and Market Weakness. In the wine sector, while there is optimism regarding the quality of this year's harvest, growers face significant challenges. The market has seen sluggish demand in the past several years, influenced by changing consumer preferences and economic pressures that have dampened wine sales across various price segments. Particularly, red grapes have struggled, with many remaining unsold after harvest. Experts suggest that to stabilize the market, it may be necessary to remove a portion of the grape acreage to better align supply with the reduced demand. This process could help alleviate the excess inventory issues that growers are currently facing, ultimately leading to a more balanced marketplace.

Table Grapes: Positive Signs. Table grapes, have seen a notable increase in shipments, with U.S. domestic shipments rising by 20% compared to last year due to larger supplies from storage. This boost is largely attributed to a recovery from last year's early harvest disruptions caused by rain, resulting in better quality grapes this season. However, this increase has led to lower shipping point prices compared to previous years, which may pressure profit margins for growers.

Raisin Grapes: High Prices and Rising Costs. The California raisin grape market is facing challenges despite a strong price outlook for 2024. While the Raisin Bargaining Association (RBA) secured one of the highest minimum prices ever, declining acreage is contributing to a supply squeeze. Acreage reductions have been ongoing as growers shift away from raisin grapes due to water scarcity and economic pressures. This acreage reduction may support price stabilization, but production costs and competition from global raisin producers remain concerns. These dynamics highlight both opportunities and difficulties for raisin growers moving forward.

Dairy: Favorable Pricing for Producers. In the dairy sector, there's a cautious optimism. Recent trends indicate a potential upswing due to higher milk prices coupled with lower feed costs. The forecast for all-milk prices in 2024 stands at approximately $22.80 per hundredweight, reflecting a favorable pricing environment for producers. This increase in milk prices is particularly important as it provides a much-needed buffer for dairy farmers who have been grappling with fluctuating costs and the emergence of highly pathogenic avian influenza (HPAI) in the San Joaquin Valley which poses a significant risk, given the region's substantial contribution to national milk production.

Cattle: High Prices Amid Uncertainties. In California, the beef market is currently experiencing significant challenges alongside potential opportunities. The cattle inventory remains at its lowest since 1951, which has constrained supply and contributed to high beef prices, particularly for choice grade beef, which has surpassed $300 per hundredweight. This scarcity has heightened consumer demand but has also created uncertainty regarding future inventory levels and production.

Interest Rates: Are Further Cuts Coming? In September 2024, the Federal Reserve implemented its first interest rate cut since 2020, reducing the federal funds rate by 50 basis points. This decision came in response to signs of economic slowing, rising unemployment, and concerns about the burden of high borrowing costs. However, despite this cut, inflation remained slightly above target, which has tempered expectations for more aggressive cuts to come out of upcoming Federal Open Market Committee meetings in November and December.

Inflation: Rising Slower. As of September 2024, the U.S. Consumer Price Index (CPI) showed a year-over-year inflation rate of 2.4%, reflecting a steady cooling trend in inflation over recent months. This marks the lowest inflation rate since early 2021. While the overall inflation rate has decreased, core inflation, which excludes volatile food and energy prices, remains somewhat higher at 3.3%. These figures suggest that while price pressures have eased for many goods, persistent inflation in services and core categories will continue to affect consumers.

Labor Market: Not So Small Revisions. The labor market in 2024 appears weaker than previously thought due to a significant revision in job numbers. In early 2024, the U.S. Bureau of Labor Statistics revised its job creation estimates from the prior year, reducing the total by 818,000 jobs, with final revisions to be released in February 2025. This large downward revision indicates that employment growth in 2022 and 2023 was not as robust as originally reported. Such a substantial correction raises concerns about the actual strength of the labor market, suggesting that earlier optimism was overstated. It also highlights that job growth may have been more sluggish than expected, contributing to a less favorable economic outlook.

Housing Market: Elevated Prices & High Borrowing Costs Persist. The housing market is weakening due to a combination of high mortgage rates, declining affordability, and reduced demand. Mortgage rates have surged to over 7% in 2024, their highest level in over two decades, making home financing significantly more expensive for buyers. As a result, monthly payments have become unaffordable for many potential homeowners, pushing demand down sharply.

Additionally, elevated home prices, which have risen dramatically in recent years, are further straining affordability. The increase in borrowing costs has outpaced wage growth, reducing the pool of qualified buyers. This has led to lower home sales and fewer new listings as sellers are reluctant to part with their homes unless absolutely necessary, further constraining market activity. Moreover, the overall economic slowdown and uncertainties in the broader financial markets have compounded these challenges, causing homebuilders to scale back on new projects, adding to the market's overall weakness.

Delinquency Rates: On the Rise. Delinquency rates for credit cards and auto loans have been rising in 2024, reflecting increased financial strain on consumers. Credit card delinquencies, which measure late payments of 30 days or more, have reached their highest level since the Great Recession, driven by record-high interest rates and inflationary pressures squeezing household budgets. Similarly, auto loan delinquencies have also surged, particularly among subprime borrowers, as higher borrowing costs and vehicle prices make it harder for consumers to keep up with monthly payments. The Federal Reserve's aggressive rate hikes have significantly impacted these sectors, with both delinquencies expected to rise further if economic conditions continue to tighten.

Profitability for agricultural producers in the San Joaquin Valley faces pressure from both economic and regulatory challenges. The Sustainable Groundwater Management Act (SGMA) is driving reductions in water usage, leading to acreage removal in crops like almonds and tomatoes, which may help stabilize prices but also increase operational complexity. Additionally, rising production costs, labor shortages, and fluctuating input prices are squeezing margins for many producers. Navigating these economic headwinds requires careful planning, as growers balance environmental compliance with the need to remain competitive in a volatile market.

At Terra West Group, we closely monitor market conditions to help agricultural producers navigate a volatile economic landscape. The following table reflects our thought not only on the current profitability of key commodities, but also a 12-month outlook on the key factors that will effect profitability moving forward.

The agricultural landscape going in fall 2024 is marked by a blend of challenges and cautious optimism. Producers across various sectors are adapting to market pressures, environmental factors, and shifting consumer demands. Strategic planning, efficiency improvements, and proactive risk management will be essential for navigating the months ahead. As industry continues to evolve, staying informed and agile will be key to seizing opportunities and ensuring long-term sustainability.

At Terra West Group, we understand that farmers face unique challenges in today’s uncertain economic climate, and we are committed to providing comprehensive financial consulting and real estate services to support your needs. Our team specializes in helping you navigate the complexities of agricultural financing and can assist in developing tailored financial strategies that align with your long-term goals, ensuring you have the resources needed to thrive.

Additionally, our expertise in agricultural real estate can help you identify opportunities for land acquisition or lease options that maximize productivity and sustainability. We also offer insights into the local market trends and assist with property valuation, ensuring you make informed decisions on your investments. Together, we can position your farming operation for success, even in challenging economic times.

References:

Sources:

This blog was inspired by AgWest Farm Credit Monthly Market Update.

Ag Daily - ‘2024 Cattle Inventory Remains Lowest Since 1951’

Agriculture Dive - ‘Energy , Transportation, Oil Prices, and Supply Chain Challenges Affecting Agriculture’

American Vineyard Magazine - ‘Raisin Grape Market Updates, Acreage Reduction and Price Trends’

California Cattlemen’s Association

Conterra - Market Interest Rates

PGIM - Agricultural Landscape October 2024

Purdue Ag Economy Barometer

Terrain Ag - Winescape Newsletter

Select Harvest USA - September 2024 Almond Market Update

Treehouse California Almonds - Market Update October 2024

USDA Citrus Acreage Report

USDA Economic Research Service - Livestock, Dairy & Poultry Outlook October 2024

USDA Tomato Fax Report

West Coast Nut - ‘Hard Time & Hope for Pistachio Growers: Struggles on the Ground Amid Export Boom’

Terra West Group Disclaimer:

The information provided in this communication/newsletter is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. Terra West Group does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will Terra West Group be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

About The Author

Donny Rocha is a seasoned agribusiness and finance professional whose knowledge and skills span from financial analysis to real estate, to operations, to sales and marketing. He has 20+ years of proven transactional experience executing real estate transactions and providing financial advisory services. With a foundational background in the farm credit system, commercial corporate banking, real estate, and on-farm experience, Donny brings a wealth of knowledge in agribusiness, real estate, risk management, and financial analytics.