The New Economics of Almond Production and the Pressure on Underlying Land Values

Donny Rocha | February 2026

A Structural Reset in Agricultural Economics

Over the past several years, agricultural producers across California, particularly almond growers, have been operating in a materially different economic environment. Elevated input and capital costs, combined with lower and more volatile commodity prices, have compressed operating margins and increased risk across most crop types. While farmland values have historically been less volatile than farm-level economics, these pressures are increasingly influencing land markets.

This blog introduces a deeper discussion on break-even economics and the changing cost structure of almond production, and examines how tighter margins, regulatory constraints, and rising capital intensity are reshaping farm balance sheets and, over time, land values.

The Structural Shift in Almond Production Economics

As an example of the broader pressures affecting agricultural economics across most crop types, almonds provide a useful case study.

Recent industry analysis points to a fundamental shift in almond production economics. While almond prices have recovered from the lows experienced in 2022, rising from approximately $1.40 per pound to the mid-$2.50 range, this improvement has been largely offset by rising input, labor, and financing costs.

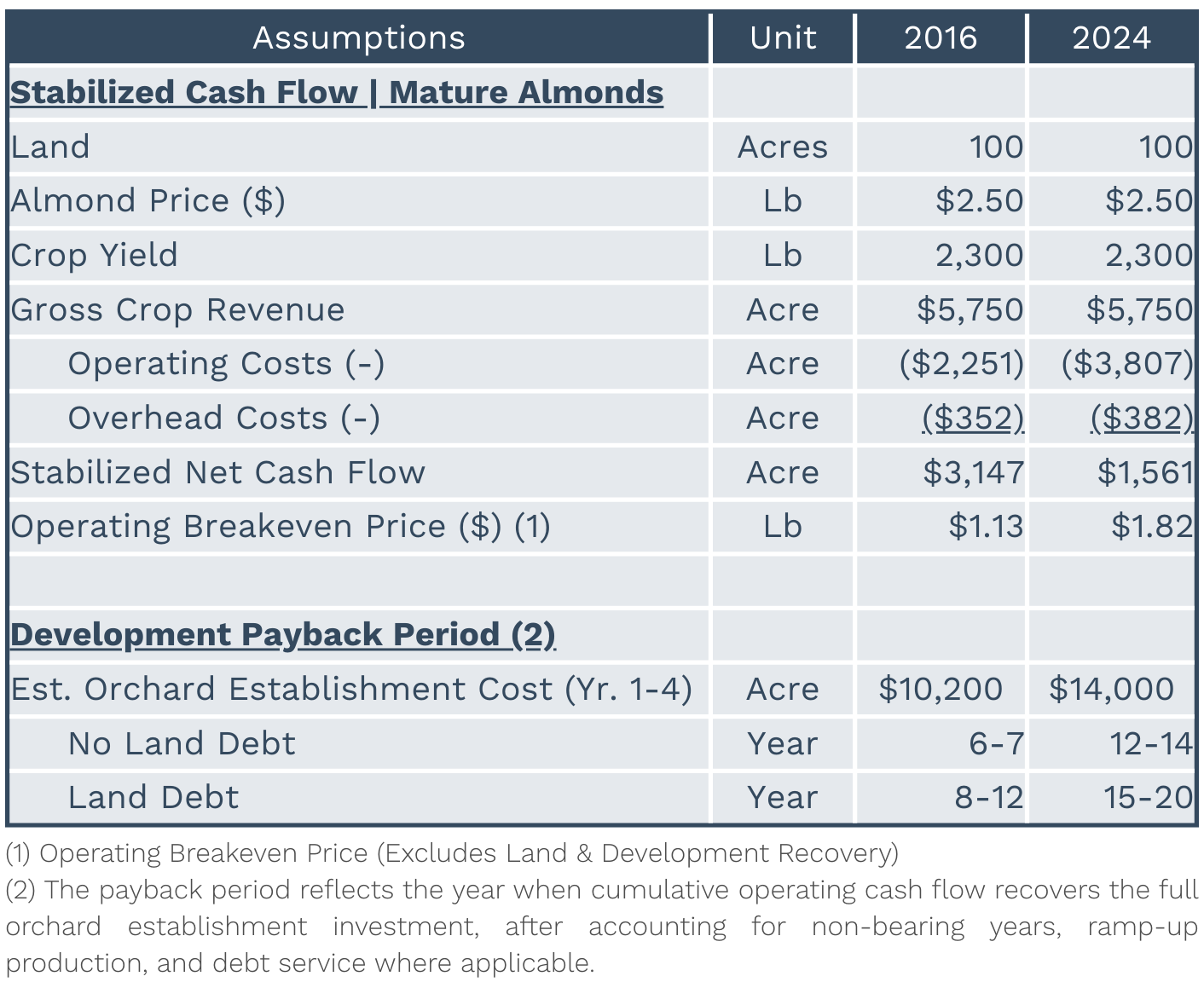

Cost benchmarks from UC Davis illustrate the magnitude of this shift. Annual almond operating costs (excluding overhead) in the northern San Joaquin Valley increased from approximately $2,251 per acre in 2016 to roughly $3,807 per acre in 2024, an increase of nearly 70%. When combined with higher interest rates and materially higher establishment costs, investment recovery timelines have lengthened significantly.

For new orchard development, cumulative establishment costs over the first four (4) years are now commonly underwritten at approximately $12,000 to $15,000 per acre (Years 1-4). These establishment costs materially shape buyer underwriting, effectively placing a practical ceiling on the combined land and development basis that can support sustainable cash flow, acceptable risk exposure, and long-term returns.

Break-Even Economics: The New Baseline

For growers evaluating new orchard development, understanding both the timing and pricing required to reach cash flow breakeven is central to assessing investment risk and long-term returns. For existing orchards, identifying the operating breakeven price is equally important, as it informs cash flow planning, capital allocation, and decisions around reinvestment or expansion.

Against this backdrop, today’s almond economics raise important questions that vary by cost structure and capital profile:

How has the time required to recover orchard development investment changed?

What pricing levels are now required for existing orchards to sustainably cover operating costs and debt service?

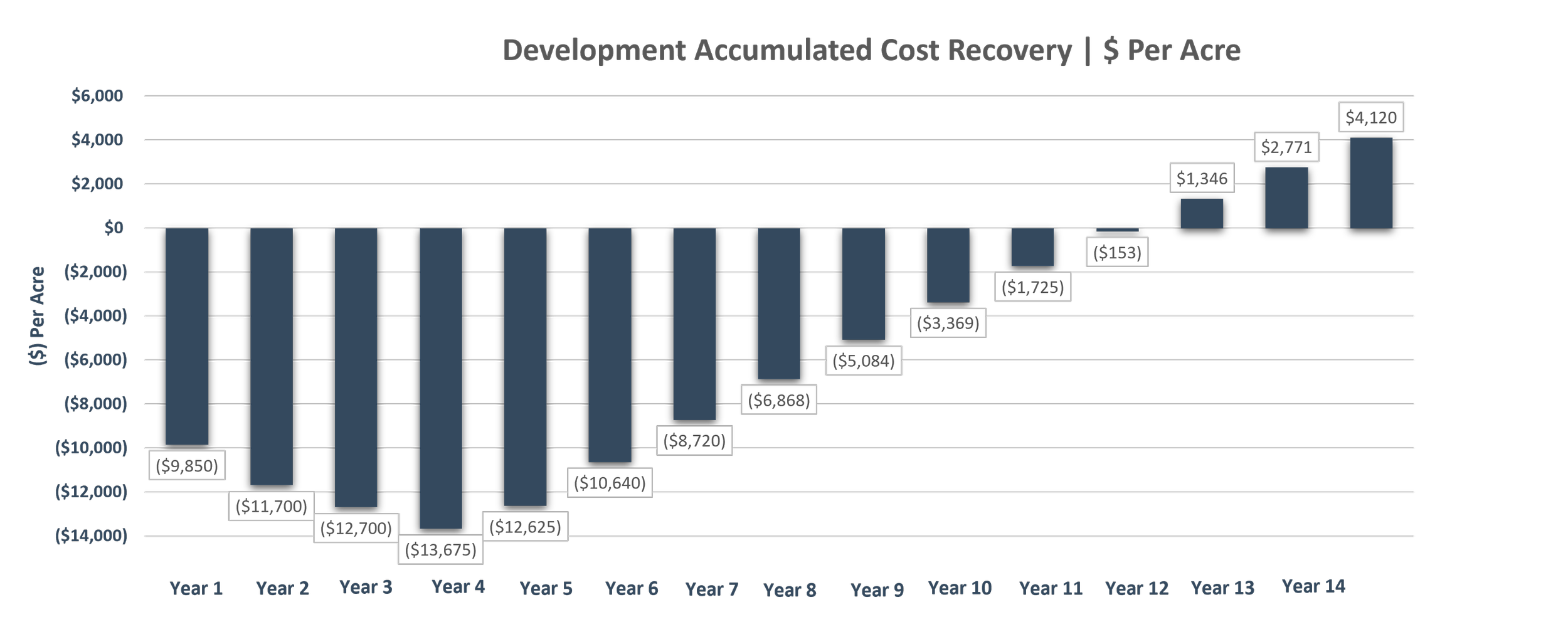

Orchard Development Payback Period (Cumulative Cash Flow Breakeven)

Evaluating orchard development economics requires a clear view of cash flow over time rather than point-in-time profitability. For this analysis, the following assumptions are used to illustrate how development payback periods have shifted under different cost and interest-rate environments:

Annual operating costs based on UC Davis cost benchmarks for the northern San Joaquin Valley in 2016 and 2024

An assumed almond price of $2.50 per pound in both periods

A land acquisition cost of $10,000 per acre (100-acre example)

Yield progression of approximately 500 pounds per acre in the 3rd leaf, 1,000 pounds in the 4th leaf, 1,900 pounds in the 5th leaf, and 2,300 pounds at maturity

A 25-year mortgage structure with 60% loan-to-value, using a 4.00% interest rate in 2016 and 7.00% in 2024

Under these assumptions, the analysis illustrates how materially longer investment recovery periods have become in the current cost and financing environment, even with the same almond price assumption.

In 2016, cumulative cash flow breakeven was reached in approximately the 6th year without land debt and the 8th year with land debt. By contrast, under 2024 cost and interest-rate conditions, breakeven extends to roughly the 12th year without land debt and may not occur until close to the 20th year when land debt is included.

While UC Davis cost studies are useful for identifying directional trends, individual operations vary materially. Actual outcomes depend on site-specific costs, yields, water reliability, financing structure, and management execution, and should be evaluated on a case-by-case basis.

Development payback periods reflect recovery of orchard establishment investment through operating cash flow. Underlying land value is evaluated separately based on long-term income potential, asset quality, and market conditions.

Operating Break-even Price

For existing orchards, my analysis shows the break-even price above operating costs for a 2,300-pound yield was $1.13 per pound in 2016 and $1.82 per pound in 2024. Including mortgage debt from the establishment analysis brings the break-even price to $1.49 per pound in 2016 and nearly $2.36 per pound in 2024, a 58% increase.

From Farm Economics to Land Values

The Cash Flow Funnel and the Quiet Pressure on Land Values

Even as almond prices improve, operating margins remain compressed due to elevated input and capital costs. This dynamic is best understood through the cash flow funnel. As revenue moves through the operation, a growing share is absorbed by operating costs, financing expense, and working capital needs before reaching the bottom of the funnel as usable cash. Over time, when too little cash reaches the bottom, debt service and reinvestment are funded by borrowing from the operating line or converting trading assets (A/R, Inventory) into cash rather than earnings.

As balance sheets tighten, land values begin to absorb the pressure. Buyers underwrite more conservatively, leverage capacity declines, and development economics place a ceiling on land pricing. The result is a narrower buyer pool and declining risk-adjusted returns for both investors and landowners.

Importantly, this adjustment is occurring unevenly across regions and assets, with well-positioned properties continuing to demonstrate resilience.

Ultimately, land values must be supported by a property’s future income potential. As buyers and operators underwrite to specific return expectations, land pricing is adjusting to align with forward-looking agricultural economics.

Farmland Values: Resilient, But Not Immune

While agricultural real estate markets have moderated from prior highs, farmland values have remained relatively resilient in many regional markets, particularly those with secure surface water supplies and limited land availability.

That said, land values have softened in regions where water constraints, cost structures, or crop economics materially impair long-term viability. This divergence has increased dispersion across farmland markets, creating both challenges and opportunities.

In today’s environment, farmland is no longer valued primarily on historical production or headline crop prices. Buyers are increasingly underwriting forward-looking economics, liquidity risk, and regulatory exposure.

Buyer Underwriting Lens, All-In Cost Ceiling

In today’s market, buyers are increasingly underwriting farmland through an all-in cost ceiling framework. Whether evaluating open cropland or an older orchard nearing the end of its economic life, buyers look at the combined land basis plus the cost to redevelop into almonds, often $12,000–$15,000 per acre over the first 4 years. That total invested capital must support manageable cash flow, acceptable risk exposure, and reasonable long-term returns, creating a practical ceiling on land pricing and placing downward pressure on open cropland values.

A similar framework applies to properties with older orchards approaching the end of their economic life. Buyers evaluate not just current production, but the cost to remove, redevelop, and carry the operation through non-bearing years. When those redevelopment costs are layered onto the land basis, total invested capital must still pencil, often requiring more conservative land valuations to maintain economic viability.

What This Means for Sellers

Farmland valuation is increasingly driven by forward-looking cash flow durability rather than historical production results alone. Buyers today are underwriting higher establishment costs, longer break-even timelines, tighter liquidity, and greater regulatory risk. Understanding how these factors compress cash flow, even in profitable operations, is essential to setting realistic expectations and optimizing sale outcomes.

For landowners considering a sale, understanding the economics faced by operators and buyers is critical. Valuation is increasingly driven by:

Realistic break-even pricing and timelines

Water reliability and regulatory exposure

Capital intensity and development feasibility

Cash flow durability, not just gross revenue potential

Anticipated ROI

Market Inefficiency Creates Opportunity

Today’s farmland market is increasingly segmented. Differences in water access, cost structures, and development feasibility are driving wider spreads in land values, rewarding disciplined underwriting and asset selection.

With new almond plantings slowing, opportunities may emerge for operators able to develop orchards efficiently. In this environment, cost discipline, yield performance, and execution advantages have become increasingly important to long-term success.

Closing Perspective

The new economics of almond production and other crop types reflect a broader shift across agriculture: profitability, liquidity (working capital) and land values are closely linked. Higher costs, tighter margins, and regulatory pressure may not immediately disrupt farmland values, but over time they place meaningful pressure on the underlying land.

Understanding break-even economics and cash flow is no longer optional, it is essential for everyday operations, forming a valuation to strategic planning, and successful transactions in today’s agricultural land market.

At Terra West Group, we help landowners, operators, and investors evaluate agricultural properties through the same economic lens used by today’s buyers and lenders. Whether you are considering a sale, redevelopment, or simply seeking clarity on how current market conditions affect your land’s value, our team provides clear, data-driven insight into property economics and valuation.

Positioning your asset with this understanding can make a material difference in outcome.

Development payback period - assuming no land debt.

Terra West Group Disclaimer:

Disclaimer: While the information contained in this report is accurate to the best of our knowledge, it is presented “as is,” with no guarantee of completeness, accuracy, or timeliness, and without warranty of any kind, express or implied. None of the contents in this report should be considered to constitute investment, legal, accounting, tax, or other advice of any kind. In no event will Terra West Group or its affiliated Associations and their respective agents and employees be liable to you or anyone else for any decision made or action taken in reliance on the information in this report.

About The Author

Donny Rocha is a seasoned agribusiness and finance professional whose knowledge and skills span from real estate to financial analysis, to operations, to sales and marketing. He has 20+ years of proven transactional experience executing real estate transactions and providing financial advisory services. With a foundational background in the farm credit system, commercial corporate banking, real estate, and on-farm experience, Donny brings a wealth of knowledge in real estate, agribusiness, risk management, and financial analytics.